Recent Articles

Buying a Home Directly From the Seller? Read This First

Homebuying tips FSBO

Published on 06/22/2026

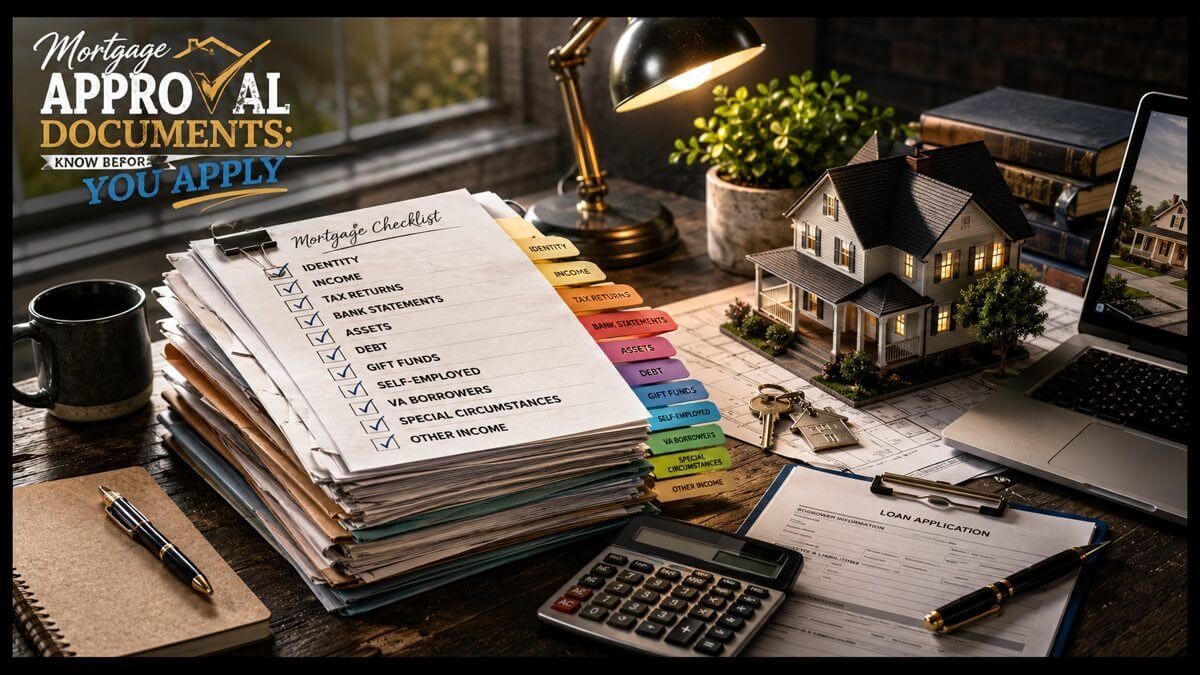

Mortgage Approval Documents: Know Before You Apply

Mortgage Approval checklist

Published on 06/11/2026

What If Rates Drop After You Lock?

What to do if rates drop after you locked your rate?

Published on 05/22/2026